The evolution of the biofuel and e-fuel production landscape

Author: Chingis Idrissov, Senior Technology Analyst at IDTechEx

Electrification is widely regarded as a leading solution for decarbonizing the on-road transport sector. However, for certain industries, electrification may not be the most viable option, leading to the growing interest in alternative low-carbon fuels like hydrogen, ammonia, biofuels, and e-fuels. In the biofuel space, biodiesel and bioethanol have historically dominated the market, but concerns about their sustainability, particularly land-use change and competition with food production, have prompted sustainable fuel producers to explore more advanced fuels like renewable diesel and sustainable aviation fuel (SAF), derived from alternative (2nd generation) feedstocks and new process technologies.

This has influenced the rise of renewable diesel, especially in regions like the US, Europe, and parts of Asia, such as China, which supply these fuels to global markets. While renewable diesel was initially produced from virgin oils, there is now a strong shift toward more sustainable feedstocks like used cooking oil, waste oils, and animal fats. These alternative sources are also gaining traction in the production of sustainable aviation fuel (SAF), offering a lower environmental footprint.

Despite the variety of existing technologies, both the advanced biofuel and e-fuel markets are still in relatively early stages of development compared to bioethanol and biodiesel. A dominant factor driving the growth of this market is regulation and policy support in key regions like the EU and the US. However, the introduction of new or improved process technologies will also cause a significant shift in the future production landscape. This article will delve into some of the key market drivers and technological developments shaping the future of advanced biofuels and e-fuels using research from IDTechEx’s new report, “Sustainable Biofuels & E-Fuels Market 2025-2035: Technologies, Players, Forecasts”.

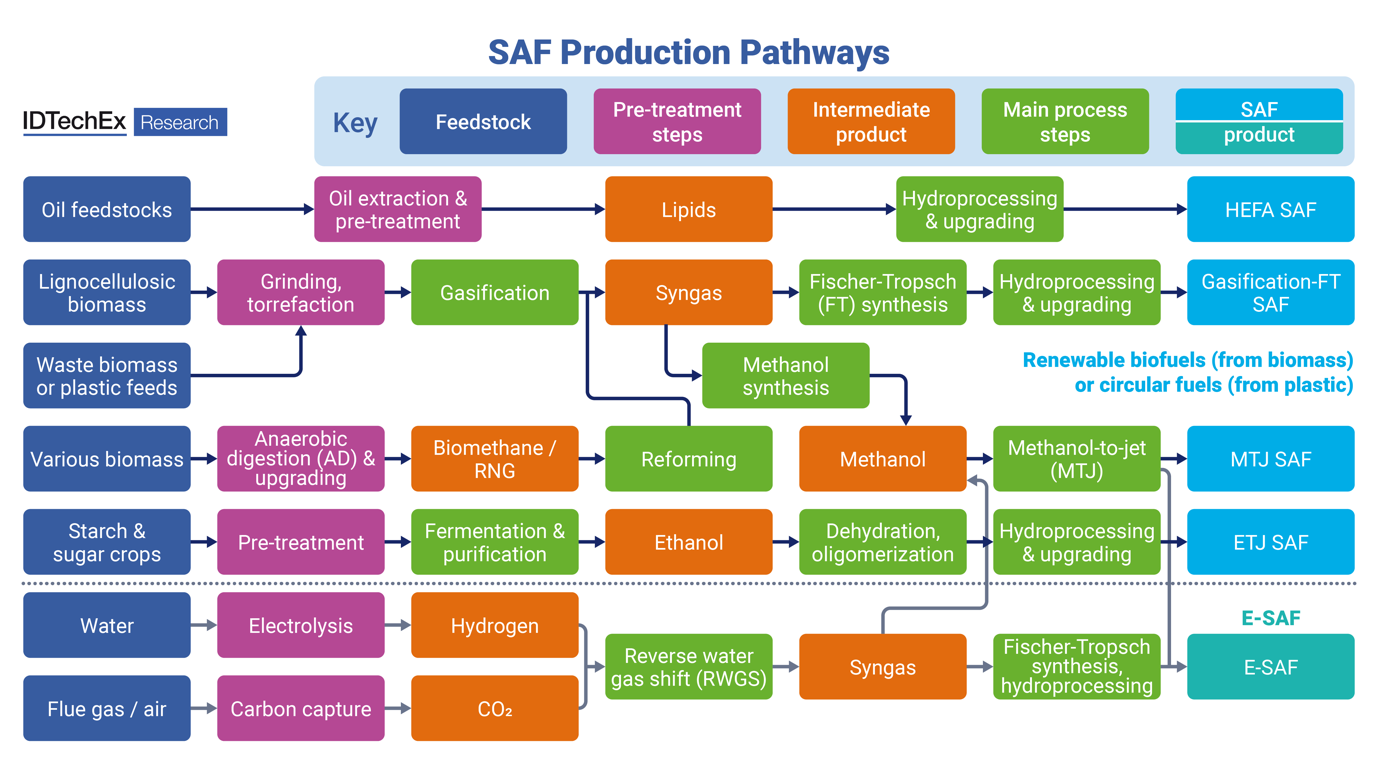

Dominance of HEFA process

The most widely used process for producing renewable diesel and sustainable aviation fuel (SAF) is the hydro-treated esters and fatty acids (HEFA) process. This process mirrors the operations in a petroleum refinery, where various fuel fractions are synthesized from crude oil. Key steps in HEFA include hydrotreating, hydrocracking, isomerization (upgrading), and fractional distillation, all of which convert the triglycerides from oil-based feedstocks into branched hydrocarbons with the right properties to be used as drop-in fuels. Due to its commercial maturity and proven reliability, most biorefineries producing renewable diesel today rely on the HEFA process.

Emergence of alternative processes & interest in SAF as a key driver of growth

The sustainable fuel landscape is evolving, and innovative technologies are gaining ground. One such advancement is the combination of gasification with Fischer-Tropsch (FT) synthesis. This process transforms waste biomass – such as agricultural and forestry residues – into synthetic hydrocarbon fuels, including renewable diesel, SAF, and gasoline. Another exciting development is the conversion of methanol and ethanol into jet fuel or gasoline, commonly known as alcohol-to-jet (ATJ) and alcohol-to-gasoline (ATG) processes. Additionally, e-fuels, which have the potential to be carbon-neutral, are generated using CO2 from the air or biogenic sources, along with water and renewable energy. These emerging technologies promise to expand the range of sustainable fuel production methods, offering alternative pathways to provide more sustainable fuels to long-haul and heavy-duty transport sectors.

The growing interest in SAF has become a significant driver of innovation in the sustainable fuel industry. This surge in attention is largely attributed to the implementation of SAF mandates in key markets. In the EU, the ReFuelEU Aviation initiative mandates a gradual increase in SAF blending, starting with 2% in 2025 and reaching 70% by 2050. Similarly, the US has introduced the SAF Grand Challenge, aiming to produce 3 billion gallons of SAF annually by 2030. These regulatory frameworks have created a strong market pull, incentivizing airlines to invest directly in technology companies and SAF production facilities. For instance, British Airways partnered with LanzaJet to build one of Europe’s first commercial-scale alcohol-to-jet (ATJ) production facilities in the UK, investing £2.5 million in the project.

Biofuel technological alternatives to HEFA are developing quickly

In recent years, cellulosic ethanol, derived from lignocellulosic biomass like agricultural residues, has garnered significant attention and investment. Companies such as Clariant have led efforts to develop plants capable of producing a more sustainable alternative to conventional bioethanol. However, despite this early promise, many companies have pulled back due to economic and technical challenges. Nevertheless, a renewed interest in cellulosic ethanol has emerged, as it is now being seen as a viable feedstock for sustainable aviation fuel (SAF) production through the alcohol-to-jet (ATJ) process. This has created fresh market opportunities. For instance, Brazilian company GranBio has partnered with Honeywell UOP to build an ATJ facility in Georgia, USA, which is expected to produce 1.2 million gallons of SAF annually.

The gasification-Fischer-Tropsch (FT) sector is also gaining momentum, with increasing commercial interest. Gasification, a mature technology primarily used to convert coal into syngas, is being adapted for biomass conversion, although it presents more challenges, such as the production of tar, which must be converted into syngas for FT synthesis. Companies like UK-based ABSL are developing innovative solutions like plasma reformers to break down tar and produce clean syngas. Additionally, FT technology, which has long been established in synthetic fuels, is seeing innovations, such as the micro-channel FT reactors being developed by companies like Velocys, aimed at increasing efficiency and enabling more compact, modular installations.

Among other innovations, technologies like pyrolysis and hydrothermal liquefaction (HTL) are also gaining attention. While pyrolysis is mainly targeted for production of biochar from biomass or recycling of plastics, HTL developers aim to use feedstocks that are conventionally hard to deal with (e.g. wastewater) and convert them into biocrude oil that can be refined into renewable diesel and SAF. IDTechEx’s report details more technological innovations and commercial insights.

Third and fourth generation biofuels face an unclear path

Third and fourth generation biofuels, derived from microalgae and other microorganisms, have long been viewed as a promising solution due to their potential to avoid competition with arable land and their ability to recycle CO2 from flue gases. Microalgae hold great potential due to their rapid growth and ability to improve cultivation efficiency. In the late 2000s and early 2010s, algal biofuels attracted significant attention and investment from major oil companies like ExxonMobil, BP, Shell, and Chevron.

Despite these early investments, algal biofuels have struggled to overcome technical and economic challenges. While research and development efforts continue in academic and start-up environments, large-scale industrial adoption remains limited. Only a few large companies are actively working on project development, and the future of algal biofuels over the next two decades remains uncertain.

E-fuels are seeing high interest globally

E-fuels, also known as power-to-liquid (PtL) fuels, are generating increasing interest globally. Produced by combining green hydrogen (generated through water electrolysis using renewable energy) with captured CO2, e-fuels offer the potential to create carbon-neutral fuels. Examples of e-fuels include e-methanol, e-methane, e-gasoline, e-diesel, and e-kerosene (also known as e-SAF).

Although second-generation biofuels currently dominate the market, e-fuels are quickly gaining traction due to their theoretically unlimited feedstock supply and carbon-neutral promise. The push from regulators, particularly in Europe and the US, alongside interest from major corporations, is accelerating the development of commercial-scale e-fuel projects. Companies like HIF Global and Infinium are leading the way, with multiple projects in development. Many of these focus on producing e-methanol and e-SAF.

E-fuel production relies on integrating multiple technologies, including direct air capture (DAC) or point-source CO2 capture, water electrolysis for green hydrogen, reverse water-gas shift (RWGS) to produce syngas, and fuel synthesis technologies like methanation and FT synthesis. Despite the maturity of these technologies, e-fuel production remains expensive, and projects face challenges like those in the renewables industry and hydrogen sector. As a result, IDTechEx predicts that second-generation biofuels will continue to lead the advanced sustainable fuel market for at least the next decade.

Summary and more insights

The sustainable fuel market is poised for substantial growth in the coming years. IDTechEx forecasts that global production capacity for renewable diesel and SAF will exceed 57 million tonnes annually by 2035. This rapid growth underscores the increasing importance of sustainable fuels in the global energy mix. While regulation will be the primary driver, growing interest from fuel end-users, such as airlines, and continued advancements in production technologies will play an increasingly significant role in shaping the market.

IDTechEx’s new report, “Sustainable Biofuels & E-Fuels Market 2025-2035: Technologies, Players, Forecasts”, provides more detailed insights into production technologies, key industry players, project case studies, and market forecasts for renewable diesel, SAF, and renewable methanol.

To find out more about this report, including downloadable sample pages, please visit www.IDTechEx.com/Biofuels.

For the full portfolio of IDTechEx research, please see www.IDTechEx.com.

Upcoming free-to-attend webinar:

Advanced Biofuels and E-Fuels: Insights Into Policy Drivers, Production Technologies, Key Innovations & Commercial Activities

Chingis Idrissov, Senior Technology Analyst at IDTechEx and author of this article, will be presenting a free-to-attend webinar on the topic on Thursday 31 October 2024 - Advanced Biofuels & E-Fuels: Insights Into Policy Drivers, Production Technologies, Key Innovations & Commercial Activities.

This webinar will summarize the current state and future directions of the sustainable fuels industry, providing key insights on the following topics:

Introduction to conventional biofuels, advanced biofuels & e-fuels

Sustainable fuel policy & market drivers

Key production technologies & pathways

Recent innovations in production technologies

Information on key market players, including technology OEMs, project developers & sustainable fuel end-users

Market outlook & summary

We will be holding exactly the same webinar three times in one day. Please click here to register for the session most convenient for you.

If you are unable to make the date, please register anyway to receive the links to the on-demand recording (available for a limited time) and webinar slides as soon as they are available.

About IDTechEx

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.